Owning investment properties brings opportunities – and responsibilities. The IRS treats money earned from leasing homes or apartments similarly to traditional wages, requiring accurate reporting. For landlords in Houston, navigating these rules can feel overwhelming without proper guidance.

This guide breaks down essential details about tax obligations for leased real estate. You’ll learn about required forms like Schedule E, deadlines for submissions, and strategies to maximize deductions. Whether managing one house or multiple units, clear knowledge helps avoid penalties while optimizing financial outcomes.

New Homes Houston Texas simplifies this process for local investors. Their team at (954) 821-4492 provides tailored advice on documentation, depreciation methods, and compliance with federal regulations. With Houston’s growing real estate market, staying informed ensures you meet obligations while protecting your investments.

Key Takeaways

- All earnings from leased properties must be reported to the IRS

- Common deductions include maintenance costs and mortgage interest

- Schedule E (Form 1040) is used to declare property-related earnings

- Tax deadlines typically align with annual filing dates

- Depreciation strategies can reduce taxable amounts over time

- Local experts help navigate region-specific regulations

Understanding Rental Income and Its Tax Implications

Leasing real estate offers financial benefits but comes with specific tax responsibilities. The IRS defines earnings from properties as any payment received for occupancy rights. This includes monthly payments, advance rent for future periods, and retained security deposits used for damage repairs. For example, Houston landlords often collect first-and-last-month payments upfront, which must be declared when received.

Defining Rental Income

Funds classified as rental property income extend beyond basic lease payments. Tenant-covered expenses, like utility bills or landscaping costs, count as taxable earnings if the agreement requires reimbursement. Even negotiated lease cancellation fees qualify. Houston’s competitive market sees many owners accepting non-refundable pet deposits – these also fall under reportable amounts.

Tax Implications Overview

Property tax deductions and operational costs can offset taxable amounts. Repairs, insurance premiums, and management fees reduce annual liabilities. The IRS allows depreciation write-offs over 27.5 years for residential buildings, a key strategy for Houston investors. However, improper documentation of security deposit handling often triggers audits.

Local regulations add complexity. Working with professionals ensures compliance while maximizing benefits like mortgage interest reductions. Subsequent sections will detail how to calculate net earnings and file documentation correctly.

How Rental Income is Taxed

Understanding federal tax obligations is crucial for those earning from leased dwellings. The IRS classifies these earnings as ordinary income, combining with wages and other sources to determine your bracket. For 2023, federal rates range from 10% to 37%, depending on total earnings.

All payments received from tenants must be added to gross income during the tax year they’re collected. This includes advance payments and non-refundable deposits. Unlike regular employment wages reported on W-2 forms, property earnings require Schedule E submissions alongside Form 1040.

Consider a landlord earning $50,000 annually from their primary job and $15,000 from a rental property. Their combined $65,000 taxable income places them in the 22% federal bracket. This blended rate applies to all earnings, emphasizing the need for accurate documentation.

State-level rules add another layer. While Texas doesn’t impose personal income tax, landlords in other states might face additional levies. Always verify local requirements alongside federal guidelines to avoid discrepancies during filings.

Proper categorization separates property earnings from passive investments like stocks. This distinction affects deductions and long-term financial planning strategies for real estate portfolios.

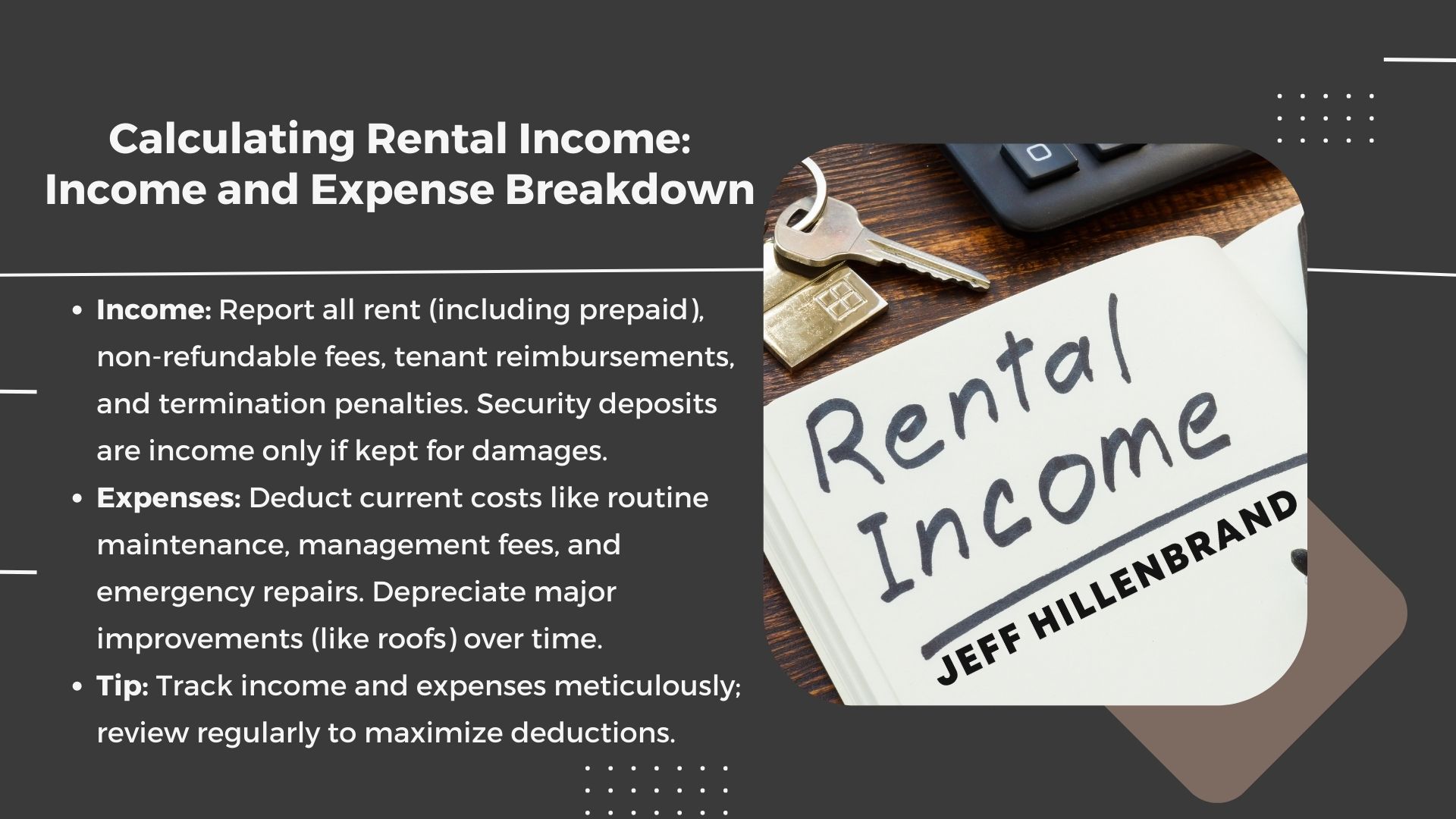

Calculating Rental Income: Income and Expense Breakdown

What exactly counts when determining your property’s financial performance? Tracking every dollar flowing in and out forms the foundation of accurate tax reporting. This process involves categorizing all earnings and operational costs – a task requiring meticulous organization.

Types of Revenue Streams

Property owners must account for various earnings beyond basic monthly payments. These include:

- Prepaid amounts for future lease periods

- Non-refundable pet or cleaning fees

- Tenant reimbursements for utilities or repairs

Security deposits only become taxable if retained for damages. For Houston landlords, lease termination penalties often represent overlooked income sources requiring documentation.

Operational Cost Reductions

Deductible expenses directly lower taxable amounts. Common examples:

- Routine maintenance like HVAC servicing

- Professional property management fees

- Emergency repair costs for storm damage

Capital improvements – such as roof replacements – require depreciation over multiple years. Using tools like QuickBooks helps separate these from immediate write-offs.

New Homes Houston Texas emphasizes digital tracking systems for real-time financial visibility. Their specialists recommend quarterly reviews to catch discrepancies early, ensuring maximum deduction eligibility during tax season.

Reporting Your Rental Income on Tax Forms

Accurate tax reporting for leased properties requires mastering key IRS forms. Proper documentation ensures compliance while maximizing potential savings through eligible write-offs. Three essential documents govern this process: Schedule E, Form 1040, and Form 4562.

Schedule E and Form 1040 Guidelines

Schedule E (Form 1040) serves as the primary document for declaring property earnings. Investors list all revenue streams here, including tenant-paid utilities and non-refundable fees. Deductible expenses fall into four main categories:

- Operating costs (repairs, insurance)

- Management fees

- Mortgage interest

- Local property taxes

This form feeds into Line 17 of Form 1040. The IRS requires net earnings calculations by subtracting total expenses from gross revenue. For example, $24,000 in annual payments minus $8,500 in costs equals $15,500 taxable amount.

| Form | Purpose | Deadline |

|---|---|---|

| Schedule E | Income/expense reporting | April 15 |

| Form 4562 | Depreciation claims | April 15 |

| Form 1040 | Total income summary | April 15 |

Reporting Depreciation with Form 4562

Form 4562 captures depreciation deductions for residential buildings. The IRS allows annual write-offs based on a 27.5-year recovery period. A $275,000 property (excluding land value) generates $10,000 yearly deductions ($275,000 ÷ 27.5).

Maintain records of improvement costs and acquisition dates. Digital tools like QuickBooks simplify tracking these figures across multiple tax years. As stated in IRS Publication 527: “Depreciation begins when the property is ready for service.”

Missing deadlines often triggers penalties. File all documents by April 15 or request a six-month extension using Form 4868. Partnering with tax professionals helps avoid calculation errors that could delay refunds or prompt audits.

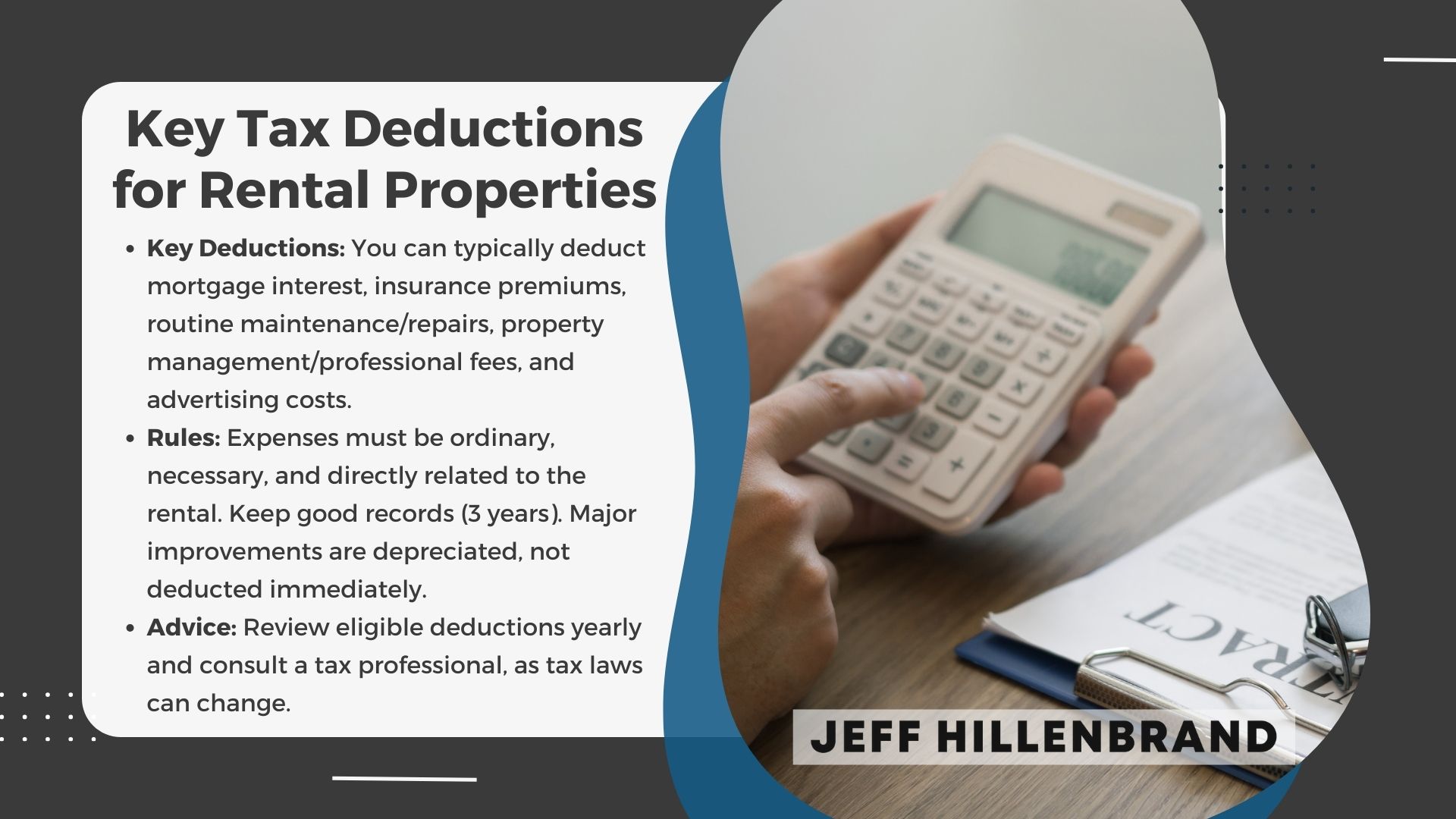

Key Tax Deductions for Rental Properties

Smart expense management transforms property investments from burdens to profitable ventures. Landlords can significantly reduce their taxable amounts by leveraging IRS-approved write-offs. Proper documentation and strategic planning turn everyday costs into financial advantages.

Mortgage Interest & Insurance Deductions

Interest paid on property loans often represents the largest deductible expense. For example, a $250,000 mortgage at 6% interest yields $15,000 in annual write-offs. Landlords can also deduct insurance premiums for homeowners, liability, and flood coverage.

These deductions directly lower property income reported to the IRS. The 2022 Tax Cuts and Jobs Act maintains this benefit, though limits apply to loans exceeding $750,000. Always retain Form 1098 from lenders as proof of interest payments.

Maintenance and Management Fees

Routine upkeep costs qualify as immediate deductions. Repainting walls, fixing plumbing leaks, and lawn care services all count. Professional fees for property managers or legal advisors also reduce taxable amounts.

Consider these deductible expenses against rent payments:

- Advertising vacancies ($200/month average)

- Emergency repairs ($1,500 storm damage fix)

- Software subscriptions for tenant screening

| Deductible | Non-Deductible | Documentation Needed |

|---|---|---|

| HVAC servicing | Personal travel | Receipts/invoices |

| Security system | Property purchase price | Lease agreements |

| Legal fees | Capital improvements | Bank statements |

These strategies help minimize income taxed while maintaining compliance. The IRS requires three years of records for audit protection. As stated in Publication 535: “Ordinary and necessary expenses must be directly related to your rental activity.”

Regularly review deductible categories when preparing your tax return. Partnering with certified professionals ensures you capture every eligible expense while adapting to regulatory changes.

Depreciation: Maximizing Your Tax Benefits

Smart property owners use depreciation to recover costs while lowering annual tax obligations. This accounting method spreads building expenses over decades, offering consistent financial advantages. The IRS requires residential properties to follow specific depreciation schedules through the Modified Accelerated Cost Recovery System (MACRS).

Depreciation Methods Explained

MACRS provides two calculation approaches:

- Straight-line: Equal deductions each year

- Accelerated: Larger deductions early, smaller later

Most investors choose straight-line for residential properties due to IRS rules. For example, a $300,000 building (excluding land value) generates $10,909 yearly deductions ($300,000 ÷ 27.5). This predictable method simplifies long-term planning.

Why 27.5 Years Matters

The IRS assigns residential properties a 27.5-year useful life based on average economic value duration. This timeframe allows:

| Advantage | Impact |

|---|---|

| Annual deductions | Reduces taxable passive income |

| Long-term savings | Lowers property taxes over decades |

| Cash flow management | Balances maintenance costs |

Land never depreciates – only structures qualify. Separate land value from building costs during calculations. As stated in IRS Publication 946: “Depreciation begins when your property is ready for tenants.”

Proper depreciation strategies turn upfront investments into lasting tax benefits. Partnering with professionals ensures accurate filings while maximizing deductions allowed under federal guidelines.

Navigating IRS Tax Brackets and Filing Requirements

Tax brackets determine your obligations but often confuse property owners. The IRS uses progressive rates where higher earnings face increased percentages. For 2024, single filers face these brackets:

| Tax Rate | Single Filers (2024) | Married Filing Jointly |

|---|---|---|

| 10% | Up to $11,600 | Up to $23,200 |

| 12% | $11,601–$47,150 | $23,201–$94,300 |

| 22% | $47,151–$100,525 | $94,301–$201,050 |

Understanding Federal Rate Structures

Property earnings combine with wages to determine your bracket. If you earn $50,000 from a job and $20,000 from leases, your $70,000 total places you in the 22% bracket. Only income above each threshold gets taxed at higher rates.

Security deposits remain non-taxable unless kept for damages. The IRS treats these funds as trust money until final lease terms. Document retention carefully to avoid misclassification as ordinary income.

Report all property earnings on Form 1040 using Schedule E. The IRS requires:

- Accurate totals for all payments received

- Proper expense categorization

- Depreciation calculations for long-term assets

Late filings incur penalties up to 25% of unpaid taxes. Set calendar reminders for April 15 deadlines. As stated in IRS Publication 17: “Taxpayers must report all income unless specifically excluded by law.”

Using Accounting Software for Rental Management

Modern property management demands precision and efficiency. Digital tools simplify tracking payments, expenses, and tax documentation. Platforms like FreshBooks and Landlord Studio eliminate manual spreadsheets while reducing errors.

These solutions automatically categorize transactions from linked bank accounts. Owners may able to generate financial reports with one click, saving hours during tax season. Features like receipt scanning and mileage tracking ensure every deductible gets recorded.

Key Benefits of Specialized Platforms

FreshBooks excels in invoicing and cash flow monitoring. Landlord Studio focuses on residential rental portfolios with tenant screening tools. Both platforms offer:

| Feature | FreshBooks | Landlord Studio |

|---|---|---|

| Expense Tracking | Real-time updates | Property-specific categories |

| Tax Reports | IRS-compliant formats | Schedule E preparation |

| Mobile Access | iOS/Android apps | Offline functionality |

Automated systems flag discrepancies in residential rental earnings. Owners may able to reconcile accounts faster while maintaining audit-ready records. Cloud storage keeps data secure yet accessible from any device.

Adopting these tools transforms chaotic paperwork into organized financial insights. The result? Smoother tax filings and stronger compliance with evolving regulations.

Record-Keeping and Documentation Strategies

Strong documentation practices form the backbone of successful property management. Organized records protect against audits while maximizing eligible deductions. Without clear proof of transactions, owners risk losing thousands in unclaimed expenses or facing IRS scrutiny.

Digital tools revolutionize how landlords track financial activity. Apps like Expensify scan receipts instantly, while platforms such as QuickBooks categorize transactions automatically. These solutions create audit-ready records by syncing bank feeds and generating real-time reports.

Effective Expense Tracking

Implement these proven methods:

- Snap photos of paper receipts immediately after purchases

- Label digital files with dates and expense types (e.g., “2024-03_Plumbing_Repair”)

- Review bank statements monthly to verify categorized transactions

One Houston investor avoided $4,200 in penalties by producing watermarked timestamps for disputed deductions. Conversely, mixing personal and business costs remains a common error – always maintain separate accounts.

New Homes Houston Texas recommends quarterly documentation reviews. Their experts at (954) 821-4492 help clients implement cloud-based systems that streamline record-keeping. As IRS Publication 583 states: “Keep records for three years from filing date.”

Common Errors and How to Avoid Them

Property owners often face hidden pitfalls when managing tax obligations. Even experienced landlords can overlook critical details that impact their financial outcomes. Awareness of these common missteps helps maintain compliance while maximizing savings.

Overlooked Deductions

Many landlords miss eligible write-offs that reduce taxable amounts. Routine costs like pest control services or gutter cleaning frequently go unreported. Tenant-paid utility reimbursements and landscaping fees also qualify if specified in lease agreements.

Consider these often-forgotten deductions:

- Appliance maintenance contracts

- Professional license fees for property managers

- Bank charges for separate business accounts

Common Reporting Mistakes

Incorrect expense categorization creates audit risks. Mixing personal home improvements with property repairs leads to rejected claims. Another frequent error involves miscalculating depreciation timelines for mixed-use buildings.

| Error | Solution |

|---|---|

| Misclassified capital improvements | Separate repairs from upgrades |

| Unreported tenant payments | Track all deposits and fees |

| Incorrect expense allocation | Use property-specific accounting |

The IRS penalizes up to 20% of underpaid taxes for substantial errors. As noted in Publication 535: “Maintain clear records distinguishing personal and business use.” Quarterly reviews with certified professionals help catch issues early.

Implement digital tracking tools to automate documentation. Schedule annual consultations to stay updated on changing regulations. Proactive measures prevent costly corrections while ensuring full benefit from allowable deductions.

Integrating Tax Planning with Property Management

Successful real estate investors treat tax strategy as part of their daily operations, not just an annual chore. Combining fiscal foresight with property oversight creates a powerful system for sustained growth. This approach turns routine decisions into opportunities for financial optimization.

Aligning Long-term Goals

Proactive planning transforms reactive tax management into a growth engine. Investors who sync lease terms with IRS deadlines often:

- Capture overlooked deductions through quarterly expense audits

- Adjust pricing models based on projected bracket changes

- Renegotiate vendor contracts to maximize write-offs

Regular reviews of local regulations help maintain compliance while identifying new savings. A 2023 National Association of Realtors study found investors updating strategies quarterly saw 18% higher net earnings than annual planners.

Implement these steps for seamless integration:

- Map major expenses to corresponding tax benefits

- Set calendar reminders for deduction deadlines

- Use digital dashboards tracking income against projections

Strategic alignment protects assets while building equity. As one Houston portfolio manager notes: “Treating taxes as operational costs rather than surprises changes everything.” This mindset shift helps investors navigate market shifts while preserving profits year after year.

Strategies for Reducing Tax Liability on Rental Income

Property investors can strategically minimize their tax burden through targeted financial planning. By combining IRS-approved deductions with smart timing, owners keep more earnings while maintaining compliance.

Harnessing Qualified Business Income Deductions

The QBI deduction allows up to 20% savings on eligible business earnings. To qualify:

- Properties must generate profits exceeding basic management activities

- Owners must file as pass-through entities (LLCs or sole proprietorships)

- Total taxable income must fall below $191,950 (single) or $383,900 (joint)

For example, a Houston investor earning $150,000 annually could claim $30,000 in QBI savings. This applies after standard deductions, making it particularly valuable for mid-sized portfolios.

Optimizing Deduction Timing

Strategic expense scheduling maximizes annual savings. Consider these approaches:

| Strategy | Impact | Best For |

|---|---|---|

| Prepaying January mortgage | Shifts interest deduction to current year | High-earning years |

| Bundling repairs | Lowers taxable amount through larger write-offs | Properties needing upgrades |

| Deferring income | Reduces current-year tax bracket | Expected lower-income years |

A 2023 case study showed a Dallas landlord saving $7,500 by accelerating roof repairs into a high-profit year. Proper documentation proved critical during IRS review.

Regular consultations with certified tax professionals ensure strategies align with evolving regulations. As one advisor notes: “Tailored planning turns generic rules into personalized advantages.”

Understanding Rental Income Taxation for Houston Landlords

Navigating property earnings requires clarity and strategic action. Accurate documentation of all payments and costs remains vital for compliance. Proper use of IRS forms ensures correct reporting, while organized expense tracking maximizes deductible opportunities.

Digital tools simplify managing leases and tax rates. Platforms that automate financial records help avoid errors during filings. Staying updated on changing regulations protects against unexpected liabilities.

New Homes Houston Texas offers tailored support for Houston investors. Their experts guide clients through complex forms and expense categorization. Proactive planning with local professionals often leads to better financial outcomes.

Review your current strategies against these insights. For personalized assistance, contact New Homes Houston Texas at (954) 821-4492. Their team transforms challenging obligations into manageable, profitable processes.